Millions of Americans rely on the federal government to cover the cost of college. Education loans have existed for generations, but borrowing only really took off in the past two decades.

Soaring college costs, higher enrollment, changes to the federal lending system, labor market demand for credentials and paltry wage growth have all contributed to the $1.6 trillion in outstanding federal student debt. This does not include debt originated in the private market. The federal lending system, which originates the vast majority of student loans, is complex. There are many moving parts and many people whose lives it has touched.

Public awareness of education debt is high amid debates over loan forgiveness. Critics of broad cancellation through presidential executive order say the policy would disproportionately benefit elites, while proponents say the student loan burden is far more nuanced.

Here’s how the debt shakes out.

The Washington Post graphic

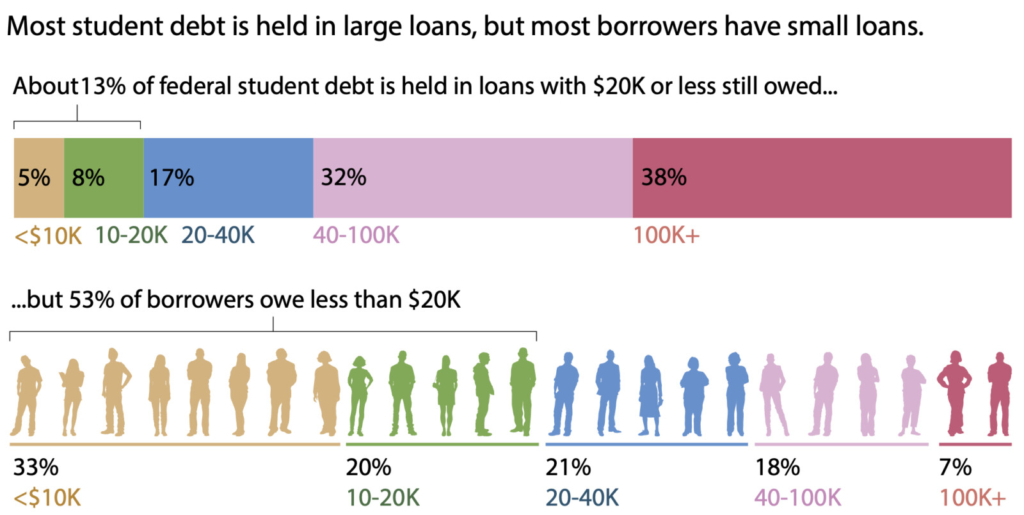

How does the debt break down?

About 1 in 5 Americans hold student loans. More than half of those 45 million people with federal student loans have $20,000 or less to pay, with about a third of all borrowers owing less than $10,000. Seven percent of people with federal debt owe more than $100,000.

Economists at the Federal Reserve say borrowers with the least amount of debt often have difficulty repaying their loans, at times because they did not complete a degree. Conversely, people with the highest loan balances are often current on their payments likely because of their higher education levels and associated earning power, according to the Federal Reserve.

Those higher balances account for nearly 40% of the $1.6 trillion in outstanding federal student loans. Borrowing for graduate degree programs has been a primary driver of the growth in federal lending. Whereas borrowing for undergraduate degrees declined by $15 billion from the 2010-11 academic year to 2017-18, it increased for graduate programs by $2.3 billion during that period, according to the National Center for Education Statistics.

Who holds student debt?

Student debt is most prevalent among Americans aged 25 to 34. Sixty-seven percent of student loan borrowers are under 40, according to the New York Federal Reserve, but only 57% of balances are owed by those under 40. In other words, people with larger balances are more likely to be older likely due to borrowing for graduate school.

Among the fastest-growing categories of student loan borrowers over the past two decades are Black students and people ages 50 and older, according to the most recent Federal Reserve data. The median income of households with student loans is $76,400, and 7% of borrowers are below the poverty line.

The Washington Post graphic

Where did the money go?

Although a majority of college students attend public two- and four-year institutions, about half of outstanding student debt is held by people who went to private schools. Among those private schools, for-profit colleges account for 17% of the debt while private nonprofit universities account for another 34%.

People who attended for-profit colleges were more likely to struggle to repay their loans than others, according to the Federal Reserve. Fed economists say high costs and low returns to for-profit enrollment generate worse student debt and repayment outcomes. They found more than one-fourth of borrowers who attended for-profit schools were behind on payments, compared with 10% who went to public institutions and 5% who attended private not-for-profit institutions.

The Washington Post graphic

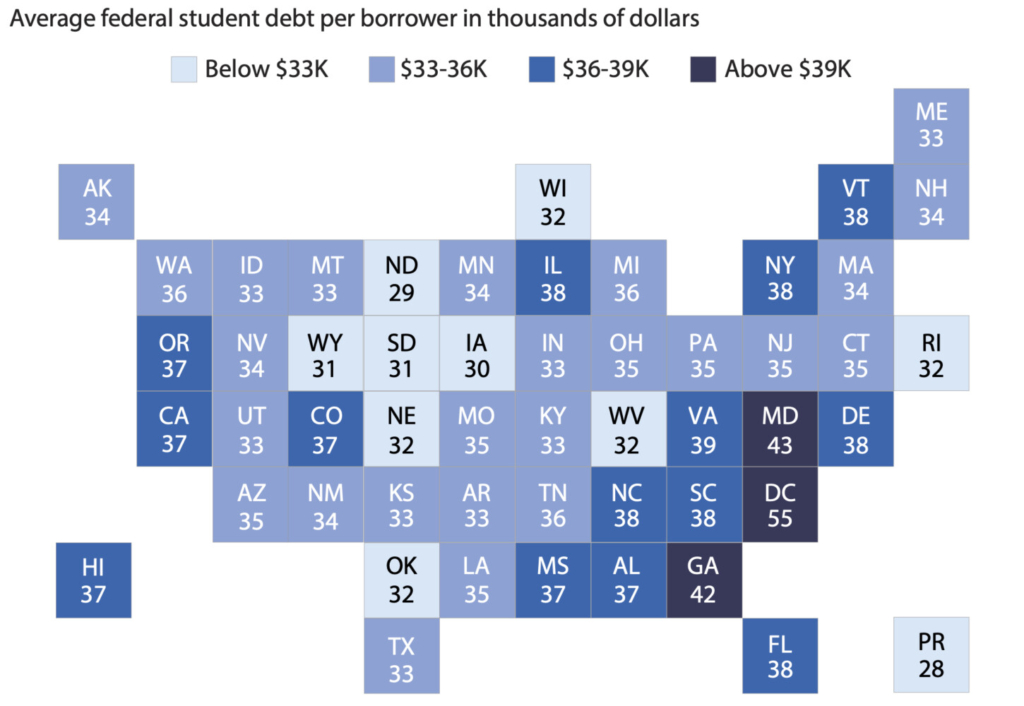

Where do borrowers live?

Americans across the country are counted in the ranks of student loan borrowers, but there are some areas that have a concentration of people with high balances. Washington, D.C., takes the top seat, with the average federal student debt per borrower at $55,000, followed by Maryland at $43,000 and Georgia at $42,000.

Some states with high debt balances have a high proportion of residents with graduate degrees. Metropolitan Washington, for instance, is one of the most educated regions of the country. The District of Columbia has the highest percentage of residents with advanced degrees, while Maryland has the third-highest, according to Census Bureau data.

Average debt loads can also be a consequence of state investment in higher education. States that prioritize funding public colleges and universities, such as California and New York, have relatively lower average debt per borrower, despite having among the largest numbers of people with student loans.

The Washington Post’s Nick Mourtoupalas contributed to this report.

Graphics use data from the Federal Student Loan Portfolio, published by the Department of Education.

Send questions/comments to the editors.